For Indian families, owning a home is a cherished dream, symbolizing stability and success. Over the last two decades, home loans have played a significant role in helping millions of Indians achieve this goal. Fueled by  rising incomes, urbanization, and government incentives, the home loan market has grown to over ₹24 lakh crore by 2024 (CRIF High Mark’s “How India Lends FY24” report:,) making it an essential part of our economy.

rising incomes, urbanization, and government incentives, the home loan market has grown to over ₹24 lakh crore by 2024 (CRIF High Mark’s “How India Lends FY24” report:,) making it an essential part of our economy.

However, while home loans make owning a home more accessible, they also come with risks. Rising interest rates, inflation, and the threat of default can have lasting financial impacts. This guide provides a comprehensive roadmap for prospective homebuyers, focusing on the key factors to consider before taking a loan, the legal rights and obligations of borrowers, and strategies to effectively manage financial challenges.

Assessing Affordability: How Much Loan Should You Take?

A home loan is likely to be the largest financial commitment for most Indian families. This is why assessing how much debt you can afford is crucial to avoid financial stress.

Loan-to-Income Ratio: As a rule of thumb, your monthly EMI payments should not exceed 30-40% of your monthly income. Going beyond this threshold can lead to financial pressure, making it harder to manage other important expenses such as household needs, education, and health emergencies.

Loan-to-Income Ratio: As a rule of thumb, your monthly EMI payments should not exceed 30-40% of your monthly income. Going beyond this threshold can lead to financial pressure, making it harder to manage other important expenses such as household needs, education, and health emergencies.- Building an Emergency Fund: Before committing to a loan, ensure you have an emergency fund that can cover 6-12 months of expenses, including EMIs. This buffer is critical to help you manage unexpected life events like job loss, medical emergencies, or financial downturns.

- Planning for Future Goals: Consider how taking a home loan fits within your broader financial plan. Stretching your finances for a bigger loan can affect other long-term priorities, such as retirement savings or children’s education.

Understanding the Legal Side of Home Loans

A home loan is not just about interest rates and EMIs; it is a legally binding agreement between you and the lender. Understanding the key elements of a home loan agreement is critical to avoid unexpected surprises and protect your financial well-being.

A home loan is not just about interest rates and EMIs; it is a legally binding agreement between you and the lender. Understanding the key elements of a home loan agreement is critical to avoid unexpected surprises and protect your financial well-being.

- Loan Amount and Tenure: Choose a loan amount and tenure that you can comfortably repay. Shorter loan terms lead to higher EMIs but reduce the total interest cost, while longer tenures lower the monthly EMI but increase the overall interest burden.

Interest Rates:- Fixed Interest Rates: These remain constant throughout the loan tenure and are suitable for those who prefer predictable EMIs, especially if interest rates are expected to rise.

Floating Interest Rates: These rates fluctuate based on market conditions, which could reduce or increase your EMIs. Floating rates may work better if you are willing to accept some risk for potentially lower payments over time.

Floating Interest Rates: These rates fluctuate based on market conditions, which could reduce or increase your EMIs. Floating rates may work better if you are willing to accept some risk for potentially lower payments over time.

- Prepayment and Foreclosure Terms: Some lenders impose penalties if you want to repay your loan early. Make sure you understand these penalties and compare them against potential savings in interest before opting for prepayment.

- Repayment Schedules and Fees: Pay attention to the detailed repayment schedule and any fees, including processing fees, administrative charges, and penalties for late payments.

Legal Rights of Borrowers: Know Your Protections

As a borrower, you have specific legal rights that protect you from unfair lending practices and harassment. Being aware of these rights can help you safeguard your interests.

Consumer Protection Act (2019): This law provides a framework for addressing grievances related to unfair lending practices. Borrowers can file complaints with Consumer Forums if they feel mistreated or misled by lenders.

Consumer Protection Act (2019): This law provides a framework for addressing grievances related to unfair lending practices. Borrowers can file complaints with Consumer Forums if they feel mistreated or misled by lenders.- Banking Regulation Act, 1949 (Section 45): Borrowers have the right to confidentiality regarding their financial information, which lenders can only disclose with the borrower’s explicit consent or under legal obligation.

- Transfer of Property Act, 1882 (Section 60): Borrowers have the right to redeem their property and repay the loan before the end of the tenure. Lenders must inform you of any foreclosure penalties.

- RBI Ombudsman Scheme: If you have unresolved grievances with your lender, you can approach the RBI Ombudsman for an impartial resolution without needing to go to court.

Challenges of EMI Default: Emotional, Legal, and Financial Impacts

Defaulting on home loan EMIs can have serious consequences, from emotional stress to legal action by lenders. Understanding the possible repercussions and knowing how to handle financial distress is essential for every borrower.

Emotional and Psychological Impact: Missing EMIs can create immense stress, anxiety, and even depression. It is important to remain calm and informed, especially when facing mounting financial pressure.

Emotional and Psychological Impact: Missing EMIs can create immense stress, anxiety, and even depression. It is important to remain calm and informed, especially when facing mounting financial pressure.- Societal and Familial Pressures: In India, societal and familial expectations often add extra pressure when managing financial commitments. It’s essential to communicate openly with family members and avoid taking on unmanageable loans just to meet social expectations.

- Legal Consequences of Default: Failing to repay your loan on time can lead to severe penalties, foreclosure of your property, and damage to your credit score. This makes it harder to access loans in the future, so it’s critical to stay informed about your legal obligations.

Recommended Strategies for Borrowers: Managing Financial Distress

If you find yourself unable to meet your EMI obligations, here are some strategies to help you navigate financial difficulty:

- Stay Calm and Informed: Understand your rights, your loan terms, and the options available to you. Keeping a clear head will help you make better decisions during tough times.

- Communicate with Your Lender: Reach out to your lender as soon as you realize you may default on payments. Many lenders offer solutions like restructuring your loan or giving you a moratorium (temporary suspension of EMI payments).

Explore Moratorium Options: In times of financial distress, you can ask for a moratorium from your lender, which temporarily pauses your EMI payments. Ensure you understand the terms and eligibility criteria, as well as the long-term impact of this option.

Explore Moratorium Options: In times of financial distress, you can ask for a moratorium from your lender, which temporarily pauses your EMI payments. Ensure you understand the terms and eligibility criteria, as well as the long-term impact of this option.- Personal Loans from Family or Friends: Borrowing from family or friends can help you manage short-term financial distress, but clear repayment agreements should be established to maintain relationships.

- Refinancing: Consider refinancing your loan if better interest rates are available. Refinancing can lower your EMIs or shorten your loan tenure, but make sure you understand the fees and long-term impact of this option.

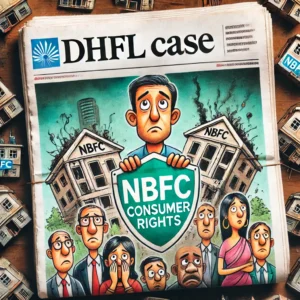

Case Study: The Dewan Housing Finance Corporation (DHFL) Crisis

The DHFL case is an important reminder of how large-scale financial mismanagement can impact borrowers:

Nature of the Case: DHFL was a major non-banking financial company (NBFC) offering home loans, but it faced allegations of fraud, financial mismanagement, and defaults on repayments in 2018. These issues created a liquidity crisis for the company.

Nature of the Case: DHFL was a major non-banking financial company (NBFC) offering home loans, but it faced allegations of fraud, financial mismanagement, and defaults on repayments in 2018. These issues created a liquidity crisis for the company.- Impact on Borrowers and Investors: The collapse of DHFL affected thousands of home loan borrowers and investors, highlighting the risks involved in borrowing from non-transparent lenders.

- Lessons Learned: Borrowers should prioritize choosing well-regulated lenders and stay informed about the financial health of their loan providers to avoid getting caught in similar crises.

Conclusion

Taking a home loan is a major step in achieving the dream of homeownership, but it also brings responsibilities ![]() and risks. By carefully assessing your financial situation, understanding your legal rights, and adopting practical strategies to manage debt, you can protect yourself from the pitfalls of default and safeguard your financial future. Open communication with your lender, proper planning, and awareness of borrower rights can help you navigate challenges and keep your dream of homeownership on track.

and risks. By carefully assessing your financial situation, understanding your legal rights, and adopting practical strategies to manage debt, you can protect yourself from the pitfalls of default and safeguard your financial future. Open communication with your lender, proper planning, and awareness of borrower rights can help you navigate challenges and keep your dream of homeownership on track.

As the home loan landscape continues to evolve, informed decision-making and proactive management of financial risks are essential for both borrowers and lenders to ensure a stable and transparent lending environment.

Kartik Krishna Panchami, Vikram 2081

October 22st , Gregorian 2024

JayA BhaaRaTa